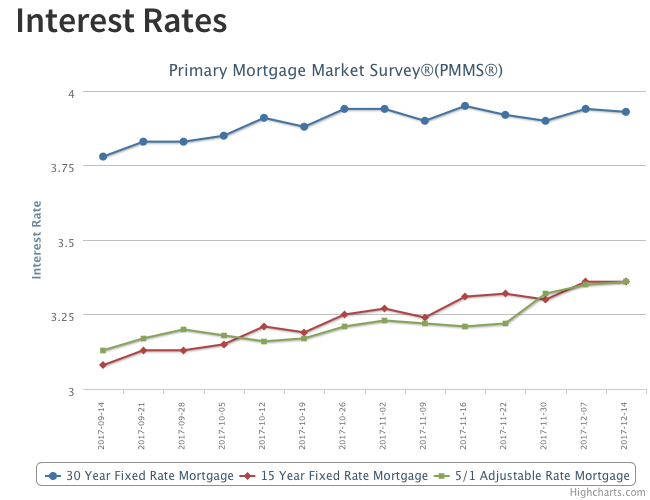

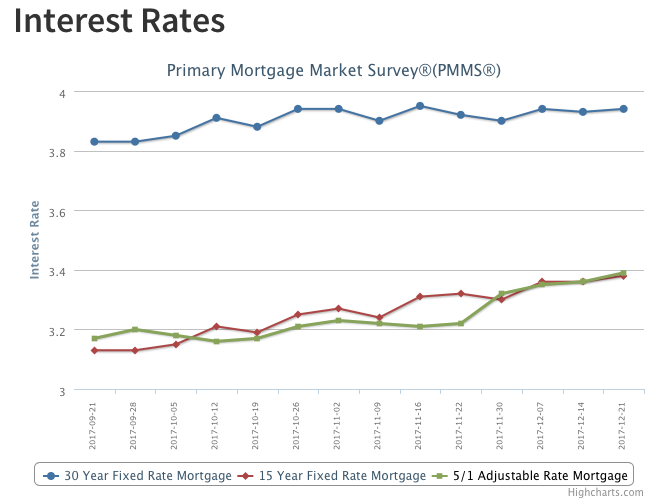

30-year fixed mortgage rates have been bouncing around in a narrow 10 basis points range since October. The U.S. average 30-year fixed mortgage rate increased 1 basis point to 3.94 percent in this week’s survey. The majority of Freddie Mac’s Primary Mortgage Market Survey® (PMMS®) was completed prior to the surge in long-term interest rates that followed the passage of the tax bill. If those rate increases stick, we’ll likely see higher mortgage rates in next week’s survey. But even with yesterday’s increase, the 10-year Treasury yield is down from a year ago, and 30-year fixed mortgage rates are 36 basis points below the level we saw in our survey last year at this time. Mortgage rates are low.