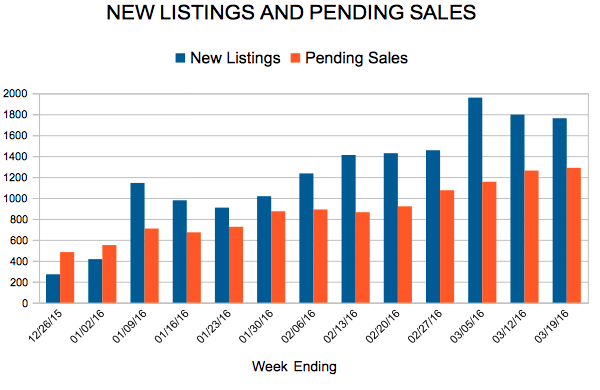

New Listings and Pending Sales

For Week Ending March 19, 2016

Heading into the spring buying season, consumers are, on average, earning higher incomes than in recent years, and there is greater trust in job security compared to last year. While these factors heighten confidence in the health of the housing market, home buyers – and especially first timers – would benefit from more inventory and slow price increases.

In the Twin Cities region, for the week ending March 19:

For the month of February:

All comparisons are to 2015

Click here for the full Weekly Market Activity Report. From The Skinny Blog.

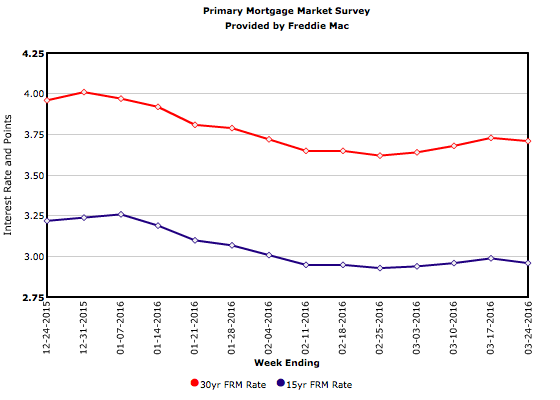

Freddie Mac’s March 24 release of the results of its Primary Mortgage Market Survey® (PMMS®) shows mortgage rates moving lower for the first time in four weeks.

For Week Ending March 12, 2016

A fresh eagerness in the warming air combined with relatively affordable prices have buyers perusing and plucking homes like spring flowers, resulting in healthy sales activity. With gas prices remaining fairly low, consumers have full tanks to visit more homes. So fluff those decorative pillows and set out the cookies for your open houses: the buyers are coming and appear to be ready to bid.

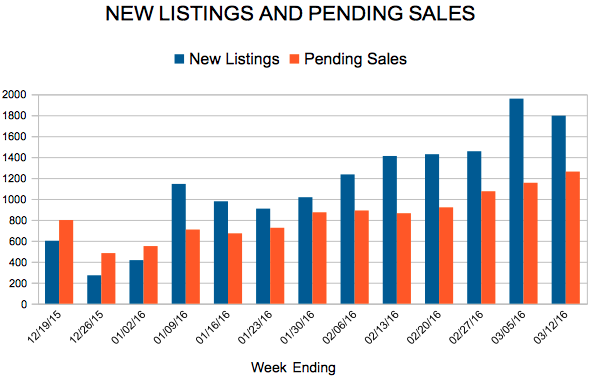

In the Twin Cities region, for the week ending March 12:

For the month of February:

All comparisons are to 2015

Click here for the full Weekly Market Activity Report. From The Skinny Blog.

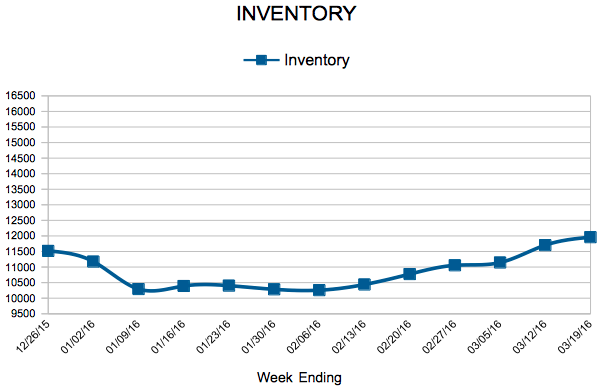

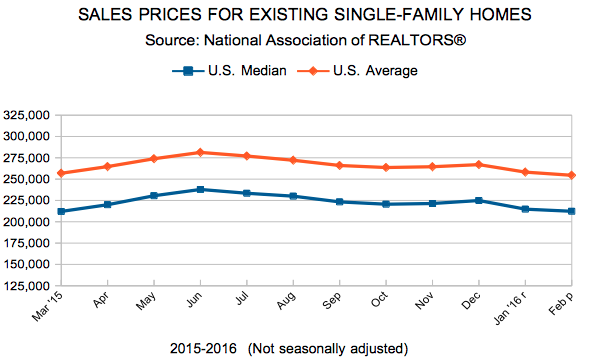

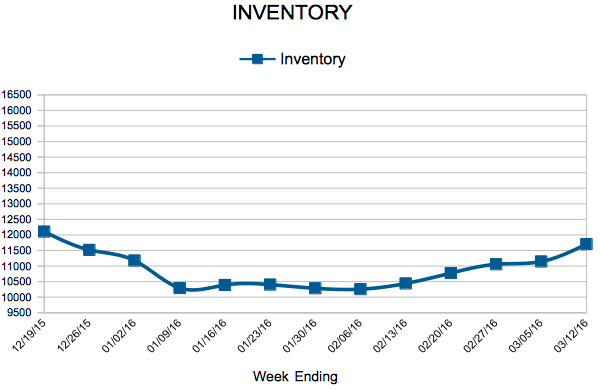

February Pending sales rose 6.7 percent while new listings increased 3.0 percent. The all-too-familiar supply crunch continued as inventory levels fell 19.4 percent to 10,953 active properties. Prices continued their steady climb back towards 2006 levels. The median sales price gained a sustainable 3.7 percent from last February and is now at $207,395. Median list price, by contrast, has already reached and exceeded its previous record, perhaps an indication that the median sales price could do the same this year.

Compared to last February, sellers accepted offers closer to their list price, as the percent of original list price received at sale was up 1.2 percent to 95.3 percent. Those offers also arrived more quickly compared to last year. Cumulative days on market declined 9.4 percent to 96 days, which is a brisk pace for a winter(ish) month. Absorption rates closely mirrored active listing levels as months supply of inventory fell 28.1 percent to 2.3 months—the second lowest figure on record, behind only January 2016. Generally, five to six months of supply is considered a balanced market. While the metropolitan area as a whole is favoring sellers, not all areas, segments or price points necessarily reflect that.

“This spring market will be a telling one for a number of reasons,” said Judy Shields, Minneapolis Area Association of REALTORS® (MAAR) President. “Many would-be buyers are waiting on sellers. Early indicators such as mortgage applications suggest demand is only likely to strengthen. The uncertainty comes on the supply side, but there’s a good chance we’ll see more inventory this year.”

It’s important to assess specific area and segment performance, since no single property spans the entire metro area nor all market segments and price points. The percentage of sales that were foreclosure or short sale fell to 16.2 percent while traditional pending sales rose 8.0 percent. Single-family homes continued to dominate sales volume, even though townhomes had the strongest increase over the last 12 months. Previously-owned sales increased 15.5 percent over the same period, compared to a 6.1 percent increase for new construction. Sales activity in the $150,000 and below range declined 9.4 percent while activity in all other price ranges is rising.

Nationally, job and wage growth trends remain encouraging. The unemployment rate continues to decline and we’re steadily producing sufficient private jobs to absorb newcomers to the labor force. Wages are growing at their fastest pace in years—an encouraging sign that should offset declining affordability brought on by rising prices and interest rates. Locally, the latest Bureau of Labor Statistics figures show the Minneapolis-St. Paul-Bloomington metropolitan area had the second lowest unemployment rate of any major metro area at 3.1 percent compared to 4.9 percent nationally. Mortgage rates are still below 4.0 percent compared to a long-term average of about 8.0 percent. Rates actually went down after the Federal Reserve’s December hike, though marginally higher rates are expected this year.

“Warmer than average temperatures have enabled home shoppers to start hunting early this year,” said Cotty Lowry, MAAR President-Elect. “Buyers appear ready for another blockbuster year, putting the charge on sellers to meet all this demand. Those considering a move would be wise to consult with a professional to better understand their position in the marketplace.”

From The Skinny Blog.